FRM: Monte carlo simulation: Brownian motion

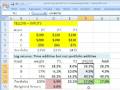

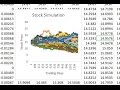

This is a classic building block for Monte Carlos simulation: Brownian motion to model a stock price. The periodic return (note the return is expressed in continuous compounding) is a function of two components: 1. constant drift, and 2. random shock; i.e., volatility multiplied by a randomized critical z value

For more great financial risk management videos, visit the Bionic Turtle website!

Видео FRM: Monte carlo simulation: Brownian motion канала Bionic Turtle

For more great financial risk management videos, visit the Bionic Turtle website!

Видео FRM: Monte carlo simulation: Brownian motion канала Bionic Turtle

Показать

Комментарии отсутствуют

Информация о видео

Другие видео канала

Monte Carlo Simulations: Run 10,000 Simulations At Once

Monte Carlo Simulations: Run 10,000 Simulations At Once FRM: Why we use log returns in finance

FRM: Why we use log returns in finance Monte Carlo Simulation of Stock Price Movement

Monte Carlo Simulation of Stock Price Movement FRM: Three approaches to value at risk (VaR)

FRM: Three approaches to value at risk (VaR) Brownian motion #1 (basic properties)

Brownian motion #1 (basic properties) 6. Monte Carlo Simulation

6. Monte Carlo Simulation FRM: Synthetic collateralized debt obligation (synthetic CDO)

FRM: Synthetic collateralized debt obligation (synthetic CDO)

FRM: Basis risk is the mother of all derivatives risk

FRM: Basis risk is the mother of all derivatives risk Random Force & Brownian Motion - Sixty Symbols

Random Force & Brownian Motion - Sixty Symbols Simulating Brownian Motion in Python

Simulating Brownian Motion in Python FRM: Bootstrapping value at risk (VaR)

FRM: Bootstrapping value at risk (VaR) FRM: Volatility approaches

FRM: Volatility approaches How to Simulate Stock Price Changes with Excel (Monte Carlo)

How to Simulate Stock Price Changes with Excel (Monte Carlo) FRM: Lognormal value at risk (VaR)

FRM: Lognormal value at risk (VaR) Monte Carlo Methods : Data Science Basics

Monte Carlo Methods : Data Science Basics Basic Monte Carlo Simulation of a Stock Portfolio in Excel

Basic Monte Carlo Simulation of a Stock Portfolio in Excel Mean Reversion and Monte Carlo

Mean Reversion and Monte Carlo Understanding and Creating Monte Carlo Simulation Step By Step

Understanding and Creating Monte Carlo Simulation Step By Step![MONTE Carlo Simulation of Value at Risk (VaR) in Python [Brownian Motion]🔴](https://i.ytimg.com/vi/11YDPyTGMnc/default.jpg) MONTE Carlo Simulation of Value at Risk (VaR) in Python [Brownian Motion]🔴

MONTE Carlo Simulation of Value at Risk (VaR) in Python [Brownian Motion]🔴