- Популярные видео

- Авто

- Видео-блоги

- ДТП, аварии

- Для маленьких

- Еда, напитки

- Животные

- Закон и право

- Знаменитости

- Игры

- Искусство

- Комедии

- Красота, мода

- Кулинария, рецепты

- Люди

- Мото

- Музыка

- Мультфильмы

- Наука, технологии

- Новости

- Образование

- Политика

- Праздники

- Приколы

- Природа

- Происшествия

- Путешествия

- Развлечения

- Ржач

- Семья

- Сериалы

- Спорт

- Стиль жизни

- ТВ передачи

- Танцы

- Технологии

- Товары

- Ужасы

- Фильмы

- Шоу-бизнес

- Юмор

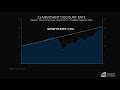

Weighting By Growth Rate vs Market Cap Increased Simulated Excess Returns

Traditional indices might weight stocks by market capitalization, potentially rewarding popularity and higher valuations. This clip introduces an alternative. Weighting by the dollar magnitude of growth.

By aligning portfolio weights with real economic contribution, this approach has improved returns and better captured the drivers of growth in backtests.

This clip is from the "Growth vs Glamour: Rethinking What Drives Equity Returns" webinar featuring Rob Arnott, Founder and Chairman of Research Affiliates.

Watch the full webinar: https://na2.hubs.ly/H05qpJ_0

-------------------------------------------------------------------------------

Note: By watching this video, you are confirming that you are employed within the financial services industry and would be viewed as an appropriate audience for this event. No retail investors should proceed.

See additional disclosures: https://na2.hubs.ly/H05dcMn0

Learn more about Research Affiliates: https://www.researchaffiliates.com

© Research Affiliates LLC. All rights reserved.

#indexinvesting #PortfolioConstruction #FactorInvesting #GrowthStrategy #AssetAllocation

Видео Weighting By Growth Rate vs Market Cap Increased Simulated Excess Returns канала Research Affiliates

By aligning portfolio weights with real economic contribution, this approach has improved returns and better captured the drivers of growth in backtests.

This clip is from the "Growth vs Glamour: Rethinking What Drives Equity Returns" webinar featuring Rob Arnott, Founder and Chairman of Research Affiliates.

Watch the full webinar: https://na2.hubs.ly/H05qpJ_0

-------------------------------------------------------------------------------

Note: By watching this video, you are confirming that you are employed within the financial services industry and would be viewed as an appropriate audience for this event. No retail investors should proceed.

See additional disclosures: https://na2.hubs.ly/H05dcMn0

Learn more about Research Affiliates: https://www.researchaffiliates.com

© Research Affiliates LLC. All rights reserved.

#indexinvesting #PortfolioConstruction #FactorInvesting #GrowthStrategy #AssetAllocation

Видео Weighting By Growth Rate vs Market Cap Increased Simulated Excess Returns канала Research Affiliates

Комментарии отсутствуют

Информация о видео

12 мая 2026 г. 3:50:25

00:03:46

Другие видео канала