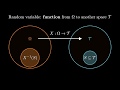

Simplified: Girsanov Theorem for Brownian Motion (Change of Probability Measure)

Explains the Girsanov’s Theorem for Brownian Motion using simple visuals. Starts with explaining the probability space of brownian motion paths, and once the probability measure is introduced, then shows how the change of probability measure looks like visually. The video ends with outlining the relationship between conditional expectation under the two measures.

Видео Simplified: Girsanov Theorem for Brownian Motion (Change of Probability Measure) канала quantpie

Видео Simplified: Girsanov Theorem for Brownian Motion (Change of Probability Measure) канала quantpie

Показать

Комментарии отсутствуют

Информация о видео

Другие видео канала

Simplified: Change of Probability Measure, and Risk Neutral Valuation

Simplified: Change of Probability Measure, and Risk Neutral Valuation Quadratic and Total Variation of Brownian Motions Paths, inc mathematical and visual illustrations

Quadratic and Total Variation of Brownian Motions Paths, inc mathematical and visual illustrations Interest Rate Term Structure Models: Introductory Concepts

Interest Rate Term Structure Models: Introductory Concepts 12 Differences between LIBOR and RFRs (alternative reference/risk free rates: SOFR, SONIA,€STR, …)

12 Differences between LIBOR and RFRs (alternative reference/risk free rates: SOFR, SONIA,€STR, …) Brownian Motion-I

Brownian Motion-I The secrets of learning a new language | Lýdia Machová

The secrets of learning a new language | Lýdia Machová Bayes theorem, the geometry of changing beliefs

Bayes theorem, the geometry of changing beliefs An illustration of Black Scholes’ Delta Hedging

An illustration of Black Scholes’ Delta Hedging LIBOR Fallback = Adj RFR + Spread

LIBOR Fallback = Adj RFR + Spread Geometric Brownian Motion: SDE Motivation and Solution

Geometric Brownian Motion: SDE Motivation and Solution Understand Calculus in 10 Minutes

Understand Calculus in 10 Minutes The Insane Biology of: The Octopus

The Insane Biology of: The Octopus An intuitive explanation the Black Scholes' formula

An intuitive explanation the Black Scholes' formula Vasicek Model Vs Cox Ingersoll Ross (CIR) Model (FRM Part 2, Book 1, Market Risk)

Vasicek Model Vs Cox Ingersoll Ross (CIR) Model (FRM Part 2, Book 1, Market Risk) Learning a language? Speak it like you’re playing a video game | Marianna Pascal | TEDxPenangRoad

Learning a language? Speak it like you’re playing a video game | Marianna Pascal | TEDxPenangRoad The Central Limit Theorem, Clearly Explained!!!

The Central Limit Theorem, Clearly Explained!!! Stochastic Calculus for Quants | Understanding Geometric Brownian Motion using Itô Calculus

Stochastic Calculus for Quants | Understanding Geometric Brownian Motion using Itô Calculus Probability spaces and random variables

Probability spaces and random variables 18. Itō Calculus

18. Itō Calculus Why dWdt=0?

Why dWdt=0?